Why are Fixed Mortgages Rates Rising Again in Canada?

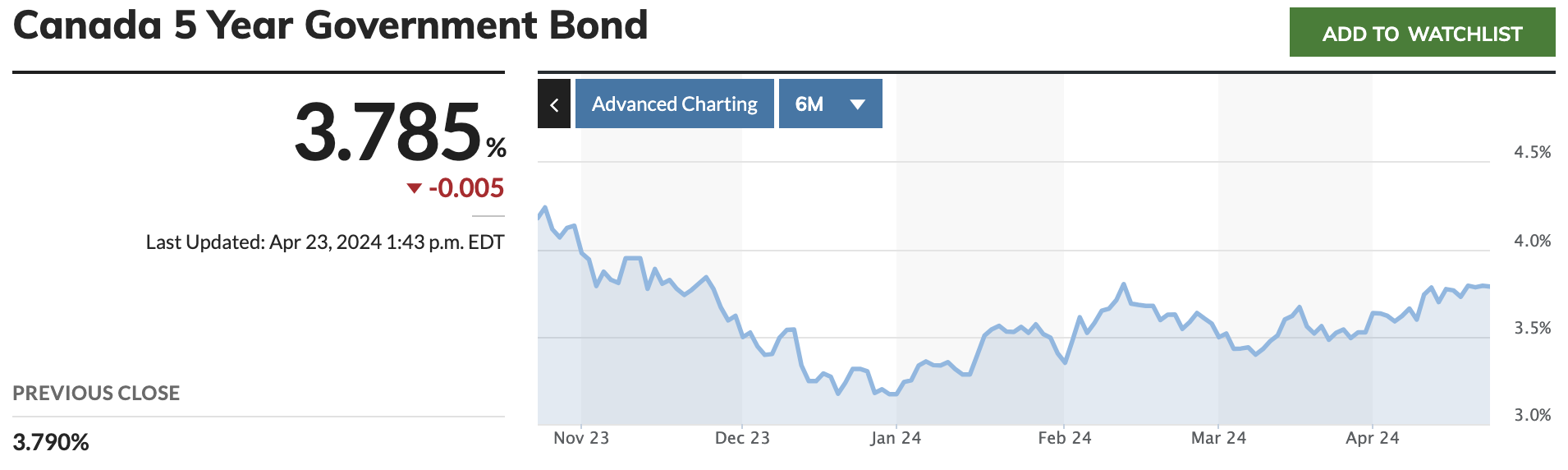

The short answer? Because the Government of Canada Bond Yields continue to rise.

The market is awaiting a drop in the key interest rate from the bank of Canada and anticipating that this could happen as early as the June or July announcement—so what’s the deal with fixed rates continuing to rise?

For fixed mortgage interest rates, It’s about more than just the BOC overnight lending rate. Fixed Rates in Canada tend to follow the Government of Canada bond yield trends and this is primarily driven by US data.

Late last year and into January, we saw a sharp decline in the Government of Canada Bond Yield, but as recent US data is showing strong employment, GDP, and inflation figures, the Canada bond yields have begun rising and taking the interest rates for fixed mortgages along with them.

So what does this mean?

These numbers indicate even if the Bank of Canada cuts the overnight lending rate, there is a possibly that we may not see the expected decline in fixed mortgage rates. Interest rates are about perceived risk, and Canada cutting rates too soon can be interpreted as a risky investment from international markets—causing bond yields to continue their increase.

Ultimately, there is room for fixed rates to rise. The gap between fixed and variable rates is still quite significant and with no clear answer to when the first key interest rate cut will actually happen, the market remains unpredictable.

What should we do if we’re purchasing a home this year?

If you’re planning on purchasing a home in 2024 you need to have a rate hold in place. Your mortgage broker can hold a rate for up to 120 days. This allows you to shop with certainty, knowing that your rate will not change. If you are nearing the end of the 120 rate hold period and you have not found a home, make sure to reach out to your mortgage broker and request a NEW rate hold and updated mortgage pre-approval.

What should we do if we have a mortgage renewing this year?

If your mortgage is renewing in the next four months, you should ensure you have a rate hold in place with another lender. Your mortgage broker can help you navigate this tricky game to ensure that you’re getting the lowest rates available at the time of renewal while keeping your hands on your current, low-interest rate until the very last day. For example, if you have a mortgage renewing with RBC, make sure to have a rate hold with another lender (say Scotiabank) so that if interest rates continue to increase and RBC is offering a higher rate at the time of renewal, you’ve hedged your bets with Scotiabank.

More questions? Reach out to our team!