April 2024 Monthly Newsletter

The Alberta housing market continues to rock and roll as we enter Spring Market.

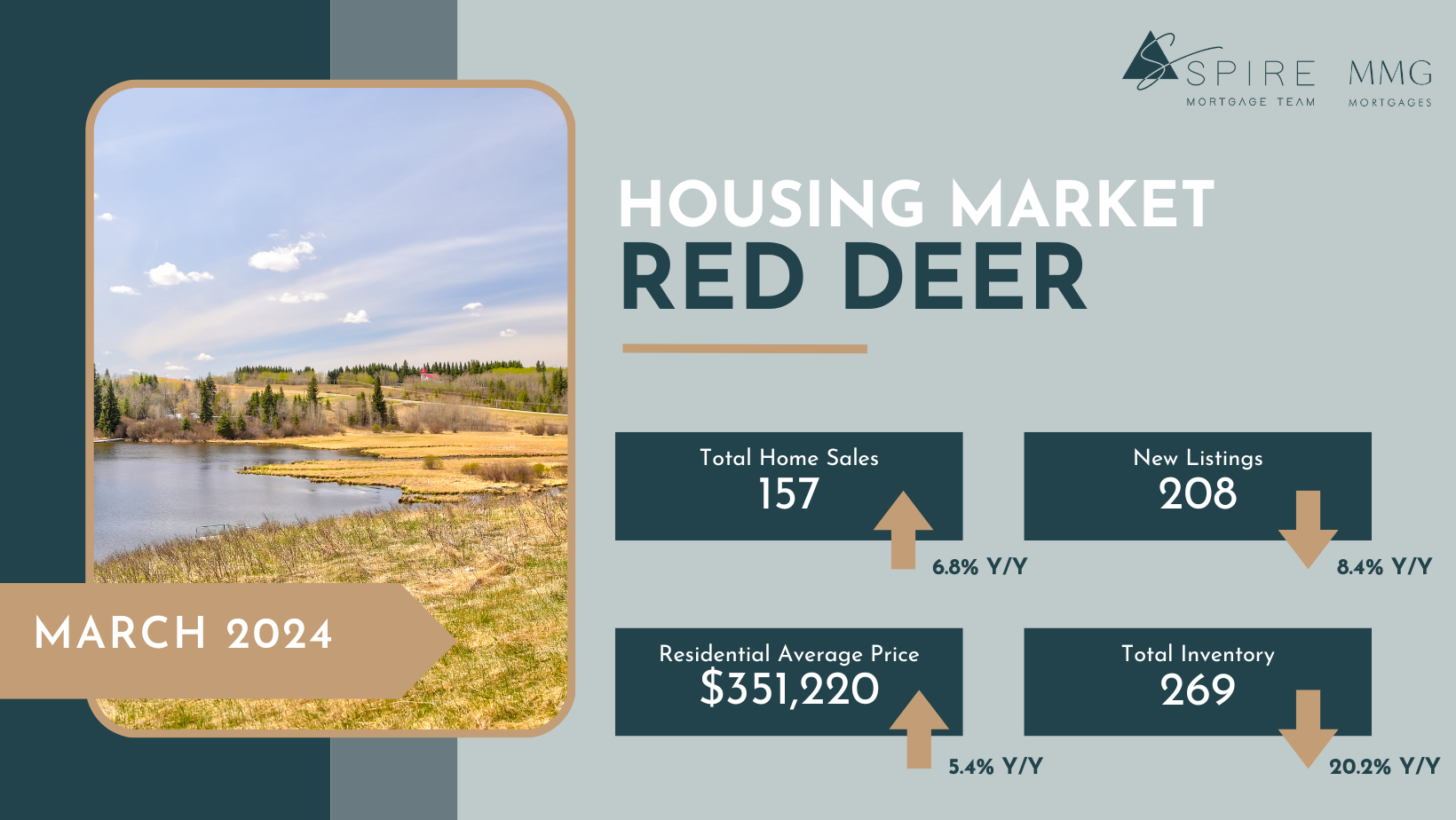

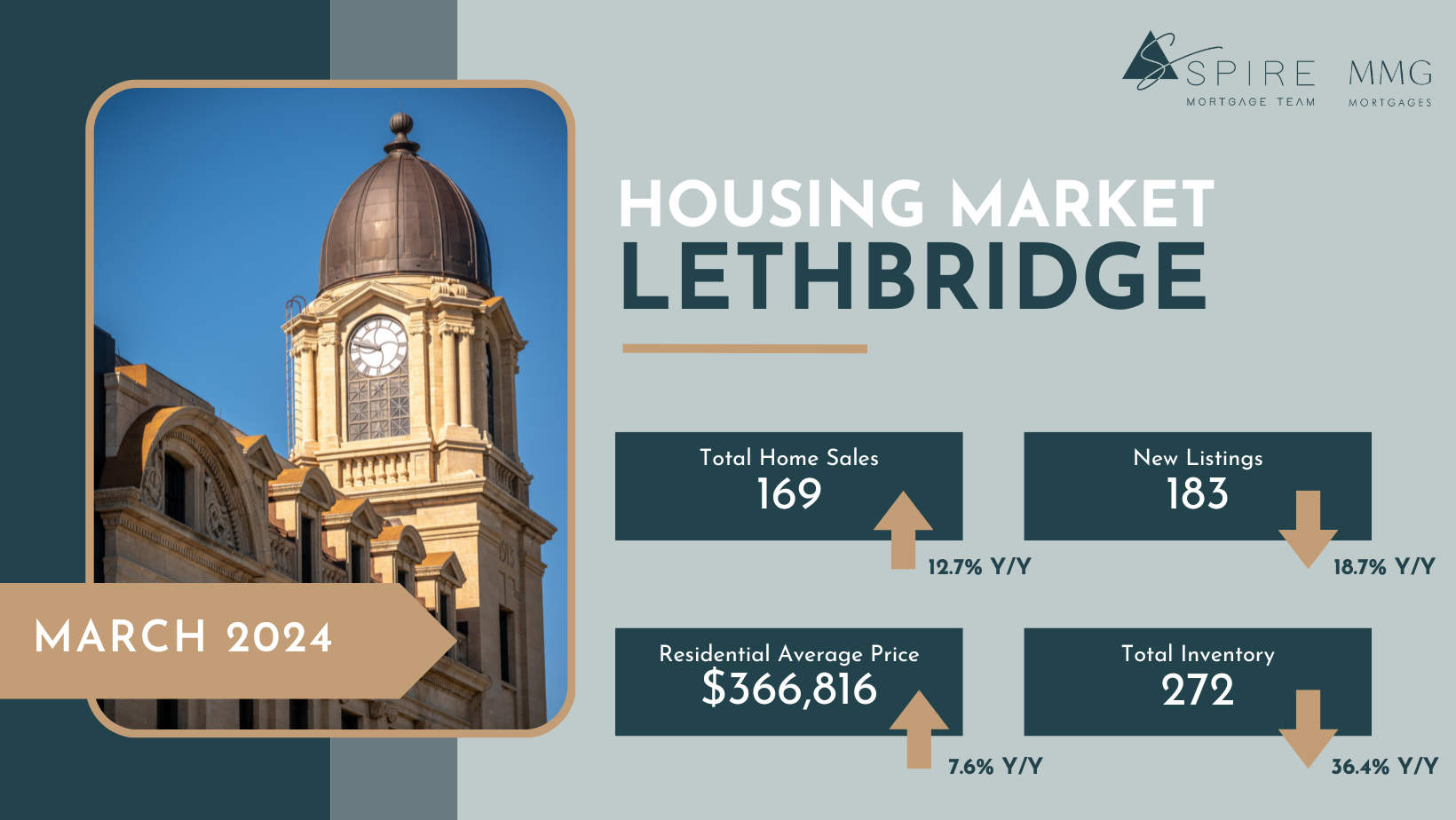

We've never had as many clients writing multiple offers (in Calgary) as we do today. I predict that as Calgary's pricing continues to increase, we will start to see it drag Edmonton, Lethbridge and Red Deer with it. We're tracking the pricing in these communities as we move through 2024, assuming we will continue to see opportunities.

We maintain that homebuyers and investors should be looking at entering the market for a few reasons:

Alberta continues to be the promised land. Strong earning potential and affordable housing make it a sweet spot for Real Estate.

Red tape in Alberta's economy (particularly in Calgary) has created a lack of supply. We believe that even with reduced immigration, Canada is short several million homes in the next 10 years.

The media falsely represents that the "big news" on the horizon in the coming months is the Bank of Canada Rate announcements. At Spire, we're not so sure. We're more interested in the 5-year government of Canada bond yield as the market tries to predict how the Canadian Government is going to deal with the:

The catastrophic lack of housing supply in Canada

The diverging Canadian and US economies

Immigration policy

I deep dive on my thoughts/opinions about the Bank of Canada announcement yesterday, the fixed rate market and the supply crisis in the 9-ish minute video below. Enjoy!

Watch Renée's April Update:

Breaking Mortgage News!

Canada to allow 30-year amortization for first-time buyers' mortgages on new home builds & $60k from RRSPs!

The government of Canada announced last week that it will allow 30-year amortization periods on insured mortgages (mortgages with less than 20% down) for first-time homebuyers purchasing newly built homes. Previously, the maximum allowed amortization for an insured mortgage was 25 years. The change will come into effect on August 1, 2024.

Here's an example of how this might change a buyer's purchasing power:

Buyers with a gross household income of $100k who are purchasing a resale home (assuming no other debt and a rate of 4.99%) will be able to purchase a home at a max price of about $425,000 and will have a monthly payment of 2,345.93.

Buyers with a gross household income of $100k who are purchasing a NEW BUILD home (assuming no other debt and a rate of 4.99%) will be able to purchase a home at a max price of about $450,000 and will have a monthly payment of 2,285.64.

Net impact: New Build vs. Resale - you can potentially purchase about $25k more house but have a payment that is $50 less each month.

The government also announced they are raising the amount first-time homebuyers can withdraw from their RRSPs -- to $60,000 from $35,000 -- to buy a home. That change will take effect on April 16, 2024.

Alberta Real Estate Market Updates

Mortgage Renewals

Less Stress, More Money.

Stay in touch with today's BEST rates! Take the stress off your list and save money in the process. Don’t just sign on the dotted line at your bank when it comes time for your renewal - know all your options!

Tell us your renewal date and as it approaches, we will make sure that you can take advantage of the best rate available.

Recent Blogs

The market is awaiting a drop in the key interest rate from the bank of Canada and anticipating that this could happen as early as the June or July announcement—so what’s the deal with fixed rates continuing to rise?